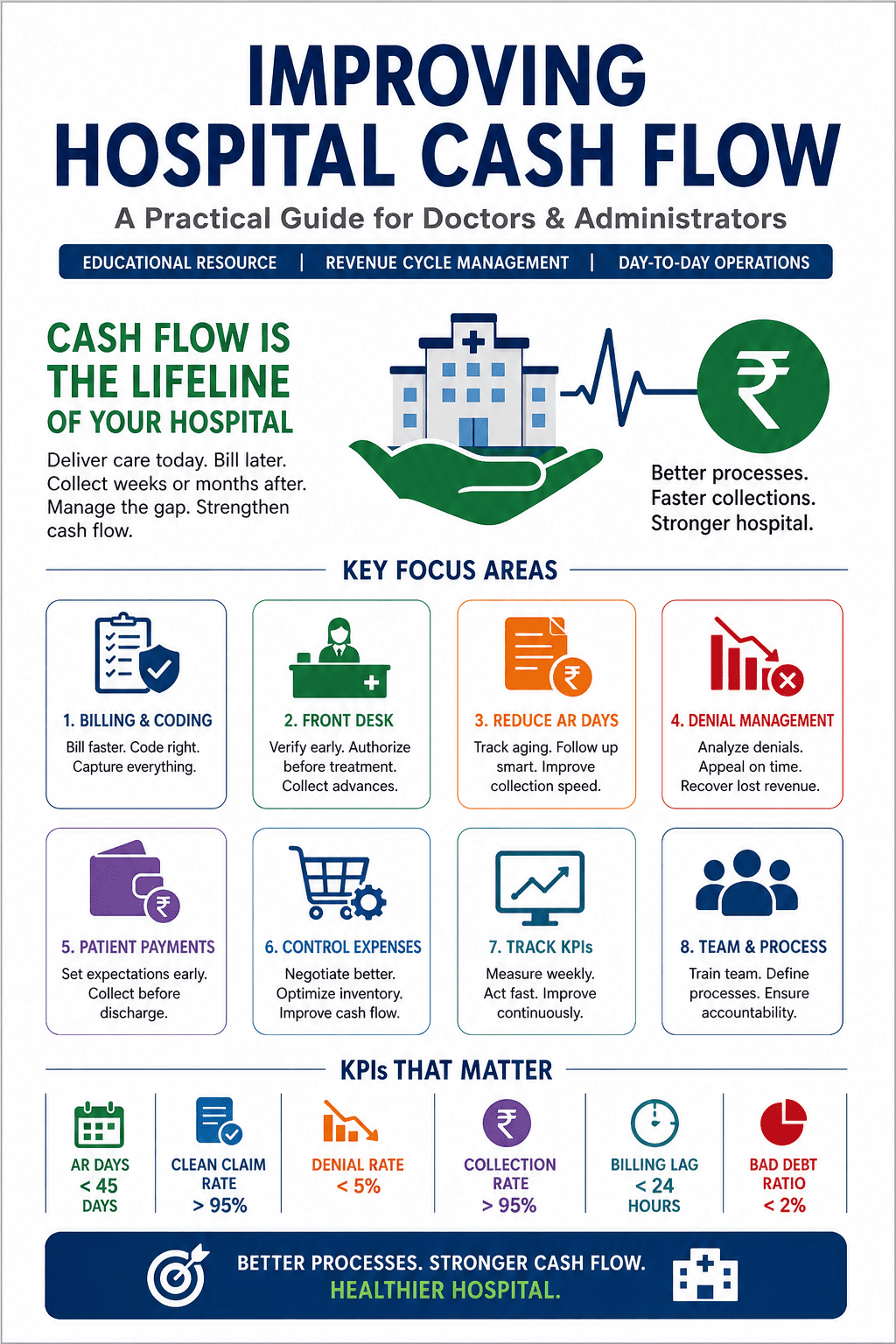

Cash flow is the lifeline of every hospital. A hospital may appear profitable on paper, yet still struggle to pay salaries, vendors, EMIs, and daily operational expenses on time. This happens because profit is shown in accounts, but cash flow decides whether the hospital can actually function smoothly every day.

Many hospitals, especially in tier-2 and tier-3 Indian cities, work with thin cash reserves while carrying 60–90 days of unpaid receivables. The biggest problem is not always lack of patients. Often, the real issue is delayed insurance settlements, unbilled procedures, coding errors, poor follow-up, weak front-desk processes, and unmanaged expenses.

A practical example: a 100-bed hospital may bill ₹80 lakhs per month but collect only ₹50 lakhs. The ₹30 lakh gap may not be true loss; it may be recoverable through better billing speed, documentation, claim tracking, denial management, and payment discipline.

1. Why Cash Flow Is the Hospital’s Lifeline

Healthcare cash flow is uniquely complex. Hospitals deliver care first, bill later, and may collect weeks or months after discharge. In some cases, payment may not come at all unless the claim is properly followed up.

This gap between service delivery and cash receipt is where hospitals silently bleed. Even a well-run hospital can face operational stress if receivables are delayed, claims are denied, or billing is incomplete.

2. The Billing and Coding Bottleneck

In many hospitals, billing happens 24–72 hours after discharge. Every hour of delay increases collection risk. A claim submitted on day one is far more likely to be paid smoothly than a claim submitted on day fourteen.

A common problem is delayed or incomplete doctor documentation. A procedure may be completed, but if notes are not written immediately, the billing team waits. If notes are incomplete, the coder may use a lower code. For example, an underbilling of ₹3,000 per case across 30 cases becomes ₹90,000 lost in a month without even appearing as a denial.

Key operational fixes include same-day or next-morning billing for all inpatient discharges, a hard 24-hour billing cutoff, EMR-integrated charge capture tools, monthly coding audits, and doctor training on documentation specificity. For example, “chest pain” and “unstable angina with NSTEMI” can significantly change coding, package rate, and claim value.

For OPD, hospitals should batch-bill at the end of the day and reconcile receipts instead of allowing scattered individual collections without proper checking.

A practical example from Mysuru: a 150-bed hospital introduced a daily “unbilled discharge” report at 8 AM. Within three months, billing turnaround time reduced from 4.2 days to 1.1 days, and monthly collections improved by ₹14 lakhs without adding new patients.

3. Front Desk: Where Cash Flow Starts or Breaks

The front desk is not only a registration counter; it is the first point of financial control. Errors made during admission often become billing problems 30 days later, when the patient has left and the insurer has raised objections.

A common example: the patient’s insurance card is taken at registration, but eligibility is not verified in real time. The patient is admitted under cashless treatment. At discharge, the TPA rejects the claim because the policy had lapsed two months earlier. The hospital then struggles to recover from the insurer or the patient.

Hospitals should verify insurance eligibility at registration every time, collect photo ID, insurance card, and authorization number before shifting the patient to the ward, collect advance deposits for all IP cases, and pre-authorize elective procedures before the surgery date.

For self-pay patients, payment expectations must be explained early, not at discharge.

Important point: pre-authorization is not guaranteed payment. The authorized amount, validity period, exclusions, and possible additional payable amount must be clearly documented and explained to the patient.

4. Reducing Accounts Receivable Days

AR days show how long it takes to collect money after billing. This is one of the most important hospital cash flow metrics. A well-run hospital should target AR days below 45. Many Indian hospitals operate at 75–120 days, meaning they carry 2.5 to 4 months of revenue as unpaid debt.

Useful AR benchmarks:

| Metric |

Target / Risk Level |

| AR Days Target |

Less than 45 days |

| Common Indian Hospital Range |

75–120 days |

| High Bad Debt Risk |

More than 180 days |

Practical AR reduction strategies include segmenting AR by payer type: self-pay, TPA/insurance, corporate, and government schemes. Each category needs a different follow-up method.

Hospitals should prepare weekly aging reports for claims above 30, 60, and 90 days. High-value claims above ₹50,000 need dedicated follow-up staff. Automatic claim status checks through NDHM or TPA portals should be used wherever possible. Genuine bad debts should be written off quarterly with proper categorization so that AR reports reflect reality.

One mid-size hospital reduced AR days from 98 to 52 in six months by splitting AR follow-up into two teams: one for TPA claims under 60 days and another for aged or disputed claims. The key was accountability and monthly collection targets for each claim bucket.

5. Denial Management: Recover Lost Revenue

Claim denial is not always final loss. It is often the beginning of an appeal opportunity. Many hospitals treat denied claims as write-offs, but 50–65% of denied claims may be recoverable if appealed correctly and on time.

Example: a TPA rejects a ₹1.8 lakh surgical claim saying the “procedure is not covered.” The billing team files it as denied. But the real issue may be wrong procedure coding. A corrected code and proper appeal could recover the amount.

Hospitals must track denial reason codes such as eligibility, coding, documentation, duplicate billing, and untimely filing. All denials should be appealed within 30 days of receipt, even if contracts allow 60–90 days.

A denial playbook should be created with common denial types, appeal templates, and required supporting documents. The hospital must also monitor the clean claim rate, which is the percentage of claims paid on first submission without correction. The target should be above 95%.

For government schemes such as Ayushman Bharat and CGHS, documentation requirements must be understood before admission and treatment, because many denials are due to missing documentation rather than service issues.

The most valuable exercise is monthly root-cause analysis of the top five denial codes. Fixing one recurring issue can prevent dozens of future denials.

6. Patient Payment Strategies

Self-pay collection is often the most difficult part of hospital cash flow. The best time to collect is before or at discharge. Once the patient leaves, recovery drops sharply.

A common issue: the patient is ready for discharge at 11 AM, but the final bill is prepared at 3 PM. The patient becomes frustrated, negotiates, pays partially, and promises to pay later. That balance then becomes a 90-day receivable with poor recovery.

Hospitals should prepare a preliminary bill 24 hours before planned discharge. High-value elective cases should have a structured schedule: 30% at booking, 30% at admission, and 40% at discharge.

UPI payment links should be sent to the patient’s mobile before discharge. EMI options through hospital-linked finance products may help patients who cannot pay in one installment. Bedside staff can also be trained to have simple financial conversations without embarrassment.

Clear itemized bills reduce disputes. When patients understand package inclusions, extras, and reasons for each charge, they are less likely to refuse payment.

7. Vendor and Expense Side: The Often-Ignored Lever

Cash flow is not only about collecting faster. It is also about controlling outflows. Many hospitals pay vendors within 15–30 days but receive insurance payments after 90 days. This creates a structural cash gap.

Hospitals should negotiate vendor payment terms of 45–60 days, especially with pharma distributors and equipment suppliers. High-value implants such as stents and joints should preferably be managed through consignment inventory, where the hospital pays only when the item is used.

Monthly inventory audits are essential because expired drugs and unused supplies are cash wasted. Department-wise expense ratios should be tracked, including OT supply cost as a percentage of OT revenue and pharmacy margin per bed.

AMCs should be renegotiated in bulk. Consolidating multiple equipment maintenance contracts with one vendor can save 15–20%.

A powerful working capital insight: extending vendor payment terms by 15 days on ₹50 lakh monthly payables gives the hospital nearly ₹25 lakh of interest-free working capital.

8. KPIs Every Hospital Should Track Weekly

Hospitals cannot improve what they do not measure. These cash flow metrics should be reviewed every week in a 15-minute finance huddle with billing, collections, and finance leadership.

| KPI |

Target |

| AR Days |

Less than 45 days |

| Clean Claim Rate |

More than 95% |

| Denial Rate |

Less than 5% |

| Collection Rate |

More than 95% of net patient revenue |

| Billing Lag |

Less than 24 hours from discharge to claim submission |

| Bad Debt Ratio |

Less than 2% of gross revenue |

Trends matter more than one-time numbers. If any metric moves in the wrong direction for three consecutive weeks, it should be treated as an early warning signal.

References and Further Reading

- Healthcare Financial Management Association — Revenue Cycle Key Performance Indicators and Benchmarks.

- American Health Information Management Association — Clinical Documentation Improvement Toolkit.

- National Accreditation Board for Hospitals & Healthcare Providers — NABH Standards for Hospitals, 5th Edition.

- Insurance Regulatory and Development Authority of India — Standardisation in Health Insurance and Claim Settlement Timelines.

- National Health Authority — Ayushman Bharat PM-JAY Operational Guidelines.

- Berwick DM, Nolan TW, Whittington J. The Triple Aim: Care, Health, and Cost. Health Affairs, 2008.

- Singh H, Misra S. Revenue Cycle Management in Indian Hospitals: Challenges and Opportunities. Journal of Health Management, 2020.