Three IMA Schemes Every Karnataka Doctor Should Know — Legal Cover, State Health, and National Health

-

Practicing medicine in India today means accepting two uncomfortable realities: a single legal notice can wipe out years of savings, and a sudden hospitalization can drain family finances even faster.

The IMA runs three schemes that address both — one for legal defense, and two health schemes (state and national) that most members don't realize can be enrolled in simultaneously for higher combined coverage.

1. IMA-KPPS — Karnataka Professional Protection Scheme

A mutual legal-defense fund for medical practitioners facing consumer complaints, professional negligence claims, and compensation demands.

What it does

- Provides protection up to ₹1 Crore per member

- Fights cases at District, State, and National Consumer Commission levels

- Covers professional negligence and CPA (Consumer Protection Act) awards

Who is covered

- Individual doctors only — not the hospitals where they practice

- Pathologists and Microbiologists are eligible — but their labs are not

Important caveats

- Membership is not automatic; it requires Managing Committee approval

- The cause of action must fall within an active membership period

- Continuous membership is mandatory to claim scheme benefits

- Members must stay in constant contact with the appointed advocate and submit case papers, investigation reports, and treatment records along with the legal notice

Cost

- One-time admission: ₹3,700

- Annual premium notice dispatched on or before April 1st each year

Contact

- 📞 9141546924 / 080-26705447

- ✉️ imakpps@gmail.com

- 🌐 www.imakppsbengaluru.org

A national counterpart — IMA NPPS (National Professional Protection Scheme) — is also available at nimapps.com for doctors who prefer national-level coverage.

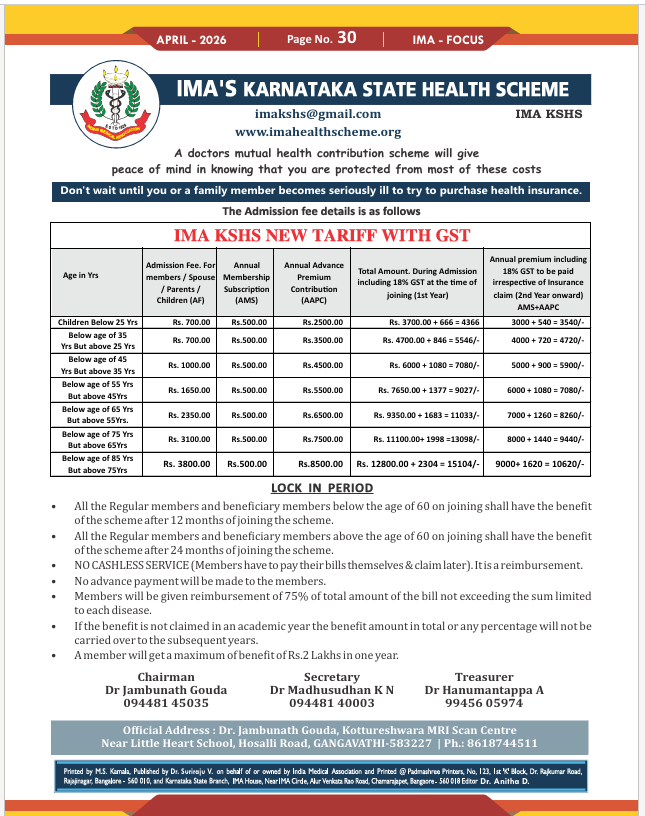

2. IMA-KSHS — Karnataka State Health Scheme

A mutual health-contribution scheme covering the member and immediate family on a reimbursement basis.

Coverage

- Member, spouse, parents, and children

- 75% reimbursement of medical bills (with per-disease caps)

- Maximum annual benefit: ₹2 Lakhs

- Reimbursement only — no cashless facility, no advance payments. Members pay first and claim later.

- Unused benefit does not carry forward to the next year

Lock-in period before claims

- Joining below age 60: 12 months

- Joining above age 60: 24 months

Premium structure (admission year + 2nd year onwards, inclusive of 18% GST)

Age band Total at admission 2nd year onwards Below 25 yrs ₹4,366 ₹3,540 25 – 35 yrs ₹5,546 ₹4,720 35 – 45 yrs ₹7,080 ₹5,900 45 – 55 yrs ₹9,027 ₹7,080 55 – 65 yrs ₹11,033 ₹8,260 65 – 75 yrs ₹13,098 ₹9,440 75 – 85 yrs ₹15,104 ₹10,620 Important: KSHS premiums escalate steeply with every age band — joining late costs significantly more over the long run.

Contact

- 📞 8618744511 / 094481 45035

- ✉️ imakshs@gmail.com

- 🌐 www.imahealthscheme.org

3. IMA-NHS — National Health Scheme

The IMA's pan-India mutual health scheme, approved by the Central Council in 2014 and operational since 2015, covering members along with their spouse, children, and parents during hospitalization.

Three things that make NHS genuinely distinctive

- Pre-existing diseases are covered from day one — including Cancer, cardiac conditions, lifestyle diseases, and Organ Transplant. Most private insurers either exclude these or impose multi-year waiting periods.

- No medical examination required to join — regardless of age or existing conditions.

- Premium does not escalate as you age within a slab. A doctor joining at 25 keeps paying the same ₹3,500 renewal until age 55. Compare this to KSHS, where every band brings a hike.

Eligibility & flexibility

- Joining age extends up to 80 years — far beyond the typical 65-year cap on other schemes

- Immediate relatives of IMA life members are also eligible

- Original bills are returned on request with a self-addressed stamped cover, so a single hospitalization can be submitted to multiple schemes

Coverage & reimbursement

- 75% of total bill reimbursed, capped at ₹2 Lakhs per year (with plans to scale up to ₹2.5–3 lakhs as membership grows)

- Treatment cost must exceed ₹5,000 to trigger a claim

- Reimbursement-only; no cashless

Premium structure

At joining (1st year, with one-time admission fee)

Age Admission AMS AFAC Total Below 25 ₹1,000 ₹500 ₹2,500 ₹4,000 25 – 35 ₹1,000 ₹500 ₹3,000 ₹4,500 35 – 45 ₹1,250 ₹500 ₹3,000 ₹4,750 45 – 55 ₹1,750 ₹500 ₹3,000 ₹5,250 55 – 60 ₹5,000 ₹500 ₹5,000 ₹10,500 60 – 65 ₹7,000 ₹500 ₹7,000 ₹14,500 65 – 70 ₹8,000 ₹500 ₹8,000 ₹16,500 70 – 80 ₹10,000 ₹500 ₹10,000 ₹20,500 Renewal (2nd year onwards — admission fee is one-time only)

Age slab AMS AFAC Total Below 25 ₹500 ₹2,500 ₹3,000 25 – 55 ₹500 ₹3,000 ₹3,500 55 – 60 ₹500 ₹5,000 ₹5,500 60 – 65 ₹500 ₹7,000 ₹7,500 65 – 70 ₹500 ₹8,000 ₹8,500 70 – 80 ₹500 ₹10,000 ₹10,500 Contact

⭐ The Most Overlooked Strategy — Stack NHS + KSHS

This is the single most underused fact among Karnataka IMA members:

NHS explicitly permits members to also enrol in other insurance schemes and State Health Schemes — and notes that combining State HS (₹3L) with National HS (₹2L) gives up to ₹5 Lakhs of total annual benefit.

For Karnataka doctors, this translates to:

- Enrol in KSHS (state) → ₹2 Lakhs coverage

- Enrol in NHS (national) → ₹2 Lakhs coverage

- File the same hospital bills under both (NHS returns originals so you can claim elsewhere)

- Effective combined cover: up to ~₹4–5 Lakhs/year

Add a separate private mediclaim policy on top of this for catastrophic-tier coverage (₹10L+), and a doctor's family is reasonably well-protected without paying enterprise insurance premiums.

Quick Comparison

IMA-KPPS IMA-KSHS IMA-NHS Type Legal protection State health National health Max benefit ₹1 Crore ₹2 Lakhs/year ₹2 Lakhs/year (₹3L target) Family covered? No Yes Yes Pre-existing diseases N/A Not explicit Covered (incl. Cancer, Cardiac, Transplant) Medical test to join N/A Not required Not required Max joining age N/A 85 80 Reimbursement rate N/A 75% 75% Cashless? N/A No No Premium escalates with age? N/A Yes (steeply) No (flat within slab) Stackable with others? N/A Yes Yes — explicitly Admission fee ₹3,700 flat ₹700 – ₹3,800 ₹1,000 – ₹10,000

Worth Discussing

A few questions for the community:

- For those enrolled in KPPS — has the legal support been responsive when you actually needed it?

- Has anyone successfully stacked NHS + KSHS on the same hospitalization? How did the dual-claim process actually work?

- KSHS vs NHS reimbursement turnaround — which is faster in practice?

- For younger doctors: enrol early in IMA schemes, or just buy comprehensive private mediclaim and skip these?

- Anyone with experience of a catastrophic claim (say >₹5L) — how did the stacking actually pay out?

If you're a Karnataka-based IMA member, all three schemes are worth a closer look — before you need them, not after.

Sources: IMA Focus bulletin, April 2026 (KPPS & KSHS details); IMA India official website — ima-india.org/ima/left-side-bar.php?pid=703 (NHS details). Please verify current figures and eligibility directly with the respective scheme offices before enrolling.